First Published Friday, February 13, 2015

Last Updated November 13, 2017

The charts below show a new housing bubble forming in California. That is not to say that a collapse in home prices is imminent. Bubbles take years to form before they burst. Moreover, they burst at different times in different regions. Lastly, while all states experience a real estate cycle, most states do not experience the dramatic price collapse associated with bubbles.

The economist Hyman Minski has written extensively on bubbles. Among other things, he identified several stages common to all bubbles (bubbles in the stock market, cattle futures, precious metals, the housing market and etc.). It's important to consider the following in identifying where the housing market is in the current market cycle;

We are currently under building. It is estimated that California needs to build in the neighborhood of 80-90,000 housing units per year more than we are currently building.

Inventory numbers remain low throughout the state and sales are at a moderate pace.

Speculators are absent from the market (I'll distinguish between speculators and investors later).

Toxic loan products are absent from the market. At the peak of the market, there were a wide assortment of loan products that offered 100% financing to borrowers with no income verification and low credit scores, teaser interests rates that later reset to rates 5% or more higher than the initial rate, low or even no down payment loans to speculators, loans with negative amortization rates, loans with large prepayment penalties and etc.

The rate of price appreciation is less than half of what it was prior to the last market collapse.

The difference between the short term cost to own and the cost to rent remains in a normal range. Here in Yuba City, the short term cost to own is about 35% more than the cost to rent a similar home. The cost to own was about 125% higher than the cost to rent at the peak of the market. The significance of this factor is that buyers will retreat from the market when the difference between to the cost to own and the cost to rent becomes too wide.

The housing market does not appear to be in any danger of a near term collapse based on the above factors. Based on the factors above, the market appears to be in what Minsky would refer to as the "Boom" or second phase of the market. It is the fifth, or "Panic" phase that sees the collapse in the market. With that in mind, home buying still needs to be viewed as a long term investment. As an example, the median home selling price in Sacramento was $217,000 in January of 2003. After the collapse, it didn't return to that level until April of 2013.

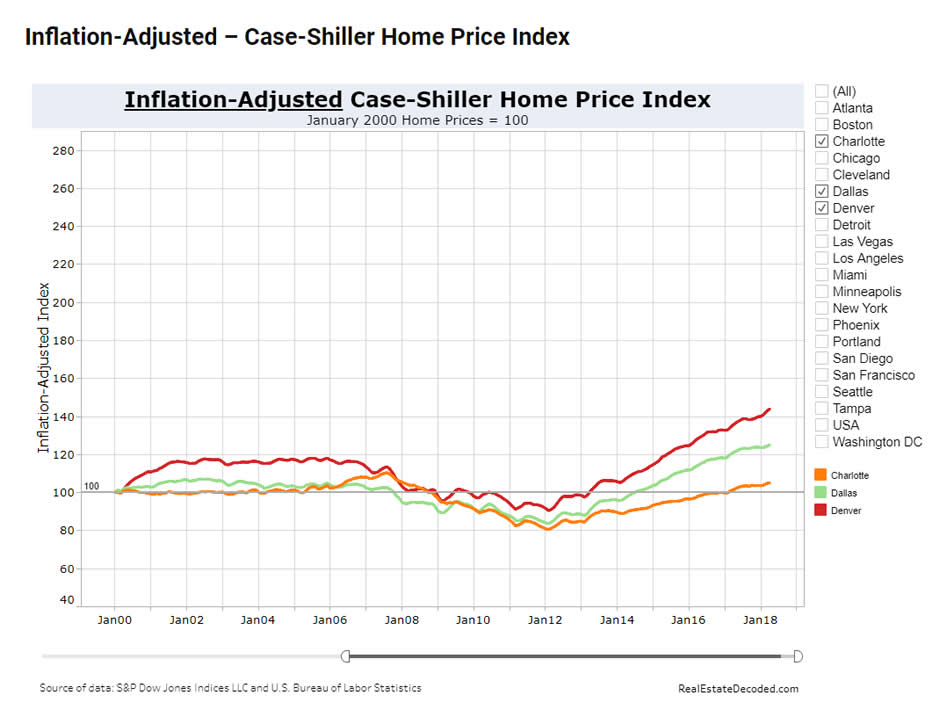

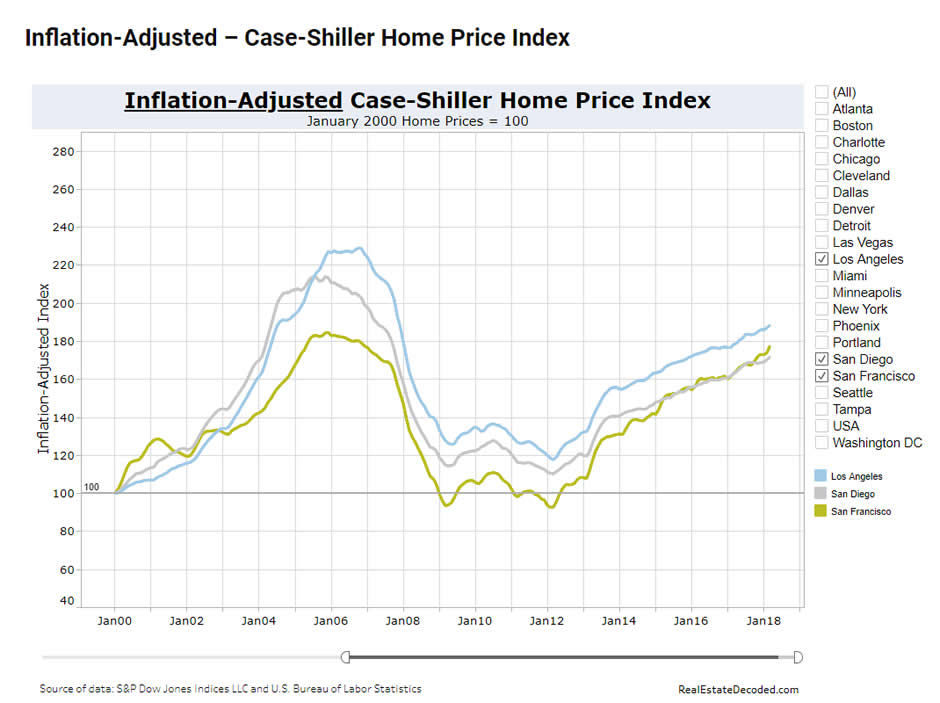

The charts below from Real Estated Decoded provide a sharp contrast. The first shows the Case-Shiller Index for three healthy real estate markets that didn't have housing bubbles in the mid 2000's (Charlotte, Dallas and Denver). The second chart shows the Case-Shiller Index for bubble prone California (Los Angeles, San Diego and San Francisco).

Chart Source: Real Estate Decoded provides an interactive chart that allows you to see trends in the other cities that make up the 20 city index. Simply follow the above link.

The next chart is our own and shows the median home prices for Sacramento and our market here in Yuba City.

Much of blame for the last housing bubble has focused on the Wall Street financial firms, lax government oversight of financial institutions, easy money policies of the Federal Reserve and loose lending policies forced by the Community Reinvestment Act. However, as Randall O'Toole wrote in his 2009 paper titled "How Urban Planners Caused the Housing Bubble", these were all nationwide in scope and yet the housing bubble only occurred in about 21 states. Most notable on the list of states experiencing bubbles were California, Nevada, Arizona and Florida.

If toxic loan products were available nationwide, why did less than half of the states have bubbles? O'Toole goes on to point out that a common element in 19 of the 21 states that had bubbles was that government created artificial housing shortages through strict growth management laws and high building fees. As an example, he cites this, "The eight counties in the San Francisco Bay Area, for example, have collectively drawn urban-growth boundaries that exclude 63 percent of the region from development. Regional and local park districts have purchased more than half of the land inside the boundaries for open space purposes. Virtually all of the remaining 17 percent has been urbanized, making it nearly impossible for developers to assemble more than a few small parcels of land for new housing or other purposes." The California Legislative Analyst's Office (LAO) has also studied the high cost of homes in California. In "California's High Housing Costs: Causes and Consequences," the LAO reported that "Over two-thirds of cities and counties in California’s coastal metros have adopted policies

(known as growth controls) explicitly aimed at limiting housing growth."

Bubbles form in response to supply shortages as demand increases. In the housing sector, the most common impediments to meeting increased demand are restrictive zoning laws, a tortuous planning process, high government fees, below market housing mandates and other government regulations such as California's Environmental Quality Act (CEQA).

When the last bubble burst, California's median home price dropped 58% from its high of $595,000 in May of 2007 to its low of $250,000 in March of 2009. The median home price in Sacramento County peaked at $380,000 in August of 2005 and hit a low of $157,115 in February of 2009 (a 59% decline). Here in Yuba City, the median home price peaked in November of 2005 at $352,950 and dropped to $129,000 in February of 2012 (a decline of over 63%).

California's planning regulations have become more stringent since 2005 so it seems only a matter of time before we experience another housing market collapse. Before that happens, we'll likely see home prices appreciate at a faster rate as lending standards are loosened and speculators enter the market. The rate of building will increase leading to an eventual over supply.

Some not so new news;

The San Jose Mercury News ran a story on July 13, 2014 titled "Bay Area home builders struggle to keep up with demand." It indicated Bay Area developers were paying $3 Million to $5 Million per acre for development land.

It ran another story on November 2, 2014 titled "Modest Bay Area homes hit mind-boggling prices." That story cited several sales of homes at "mind boggling" prices including one unspectacular 992 square foot Palo Alto home that sold for $3 Million.

The Case-Shillar index for all three California cities tracked by Real Estate Decoded (San Diego, Los Angeles & San Francisco) on it's "Case-Shiller Home Price Trends in 20 Cities" shows a bubble forming.

The number of homes listed for sale in all of Sacramento County dropped from 3,329 active listings November 1, 2014 to 2,237 active listings on February 1, 2015.

On March 17, 2015, the State of California's Legislative Analyst's Office (LAO) released its report titled "California's High Housing Costs: Causes and Consequences." The LAO report identifies a lack of supply in California's coastal communities as the primary cause of California's high housing costs. Among other things, it noted that over two-thirds of cities and counties in California’s coastal metros have adopted growth control policies explicitly aimed at limiting housing growth.

Given that over building is at least a few years away and that it takes time for loose lending standards to take effect even when they recur, it seems that we are at least a few years away from any collapse in the housing market.

A final note about bubbles: Low and middle income families suffer the most from the restrictive housing policies that set the conditions for housing bubbles. These policies put home ownership out of reach for many low and middle income families and cause rents to be artificially high. Additionally, low and middle income families are most likely to use low down payment loans and be crushed by falling home prices. This, in turn, contributes significantly to California's growing income and wealth gap.

Valuable resources for understanding the impact of government regulations on home prices are;

The housing cycle and the stages in a housing bubble...

Economist Hyman P.

Minsky identified five stages in a typical bubble cycle. These are displacement, boom, euphoria, profit taking and panic. The full real estate cycle includes some additional stages;

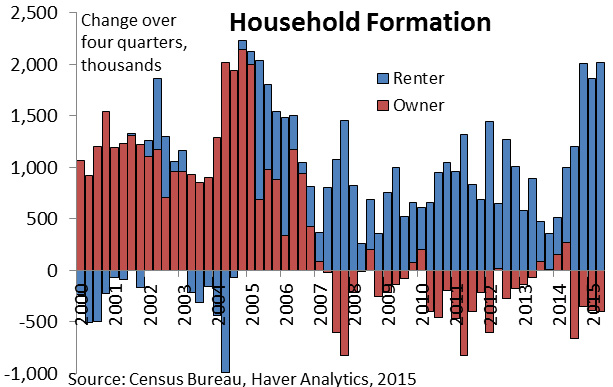

Displacement: This refers to an event or condition that changes the supply and demand relationship. In the real estate sector, common factors include increasing household incomes, lower interest rates and increasing household formation rates. As an example, The Mortgage Bankers Association reported on 4/7/2010 that "1.2 million households were lost from 2005 to 2008, despite the population increase of 3.4 million..." New household formation rates remained low and new home construction was commensurate with the lower household formation rates. Household formation rates returned to normal levels in 2014 though new home construction has not. States with restrictive housing policies, such as California, prevent the market from responding to this increased demand. This displacement puts upward pressure on prices and will increase as the economy improves and the household formation rate increases.

From Nareit comes this chart on household formation;

Boom: Home prices and rents rise slowly following a displacement but then gain momentum as more home buyers and renters enter the market. Restrictive housing policies prevent developers from quickly responding to the increased demand. During this phase, there will be widespread media coverage. Landlords will experience a dramatic increase in the number of inquiries when their rental properties become vacant. Lenders will begin loosening credit standards to allow more buyers to enter the market. Politicians will talk of a housing crisis and pass legislation enabling people who couldn't otherwise purchase homes to become buyers. In effect, lenders and politicians are adding fuel to the fire by taking action that increases demand when the problem is caused by a lack of supply.

Euphoria: During this phase, crowd logic overwhelms reasoned thinking. Home prices continue to climb rapidly and speculators enter the market. For our purposes, speculators are non-owner/occupant purchasers who are willing to take a negative cash flow with the expectation that prices will continue their rapid ascent. New valuation theories are used to justify the relentless rise in home prices. Lenders will continue to loosen credit standards. Fraud will increase.

Here in Yuba City, the Euphoria phase ended about March of 2005. By then, there were only 127 homes listed for sale. There were 119 closed sales that month. The median selling price had risen to $297,450 from about $120,000 in early 2000. A 1,052 square foot, 3 bedroom, 1 bath home in the Queens Avenue/Stafford Way area had risen in value to about $200,000 even though it would rent for no more than $950 per month. A prospective home owner using a minimum down payment FHA loan would pay a premium of about $700 per month for the privilege of owning that home. Investors with low down payment loans paid an even higher premium because the interest rates on their loans were higher.

The rise in fraud through the use of stated income or "liar loans" was rampant by both home buyers and loan officers. Pay option adjustable rate mortgage loans (ARMs) became popular. These loans permitted negative amortization. Another popular product was known as the 2/28 ARM. This included a teaser interest rate fixed for two years before resetting to an adjustable rate for the remaining 28 years of the loan. These loans allowed fraudulent homeowners that over stated their income to have more affordable payments while they hoped for a change in their circumstances. It allowed highly leveraged speculators to minimize their out of pocket losses while their much anticipated profits from appreciation materialized.

Profit Taking: Savvy investors recognize the warning signs and begin selling. Many renters, not willing to pay large premiums in order to own a home retreat from the market. Increasing inventory and decreasing sales are seen during this period. Despite increasing inventory and declining sales, valuations may reach extreme levels during this phase.

While there will be much talk of a housing bubble and a small percentage of investors will liquidate their positions, most will not. Many will argue that this is not a bubble. It was during the profit taking phase that congressman Barney Frank made his semi-famous "This is not a bubble" speech.

Sacramento County home prices peaked in August of 2005 and here in Yuba City in November of 2005. By then, there were 369 homes on the market here in Yuba City and our median home price hit $352,950. Monthly sales had fallen to 92. That 1,052 square foot home had risen in value to about $255,000 and interest rates had risen as well. An owner/occupant purchaser of the 1,052 square foot home would be paying a premium of over $1,150 per month over the cost of renting a similar home.

Panic: Home prices collapse and more buyers leave the market. Renters who were reluctant to pay the high premium for the privilege of home ownership while prices were rising sharply now find even more reason not to purchase as they watch home prices plummet. Buyers considering speculative purchases quickly back out of the market as it becomes obvious that a business model relying on rapidly increasing values is no longer valid. Lenders will tighten lending standards keeping other prospective buyers out of the market.

Six months following the peak in Yuba City home prices, monthly sales activity dropped to 52 and the median home price dropped to $294,000. The number of homes listed for sale increased to 503 by September of 2006.

Beyond the Panic: The real estate cycle does not end when the panic subsides. Highly leveraged speculators that were not able to sell find themselves trapped with under water mortgages and hoping for a recovery. Most of them will default on their loans as the futility of their situation becomes obvious. The economy will also be in decline as vast amounts of wealth evaporate. Unemployment rates rise. Household incomes decline. Many homeowners find themselves unable to make their house payments. The foreclosure and short sale processes are slow and it takes years for this to play out.

The Return of Buyers: Yuba City home buyer's began returning to the market in large numbers in the first part of 2008. By then, the value of the home near Queens Avenue and Stafford Way had declined to about $125,000. Interest rates had also declined slightly. The cost of owning that home was then $100 to $150 more than the cost of renting. The premium for owning a 1,300 square foot home near Lincoln School had declined to about $350. In spite of the near normal level of buyers and declining inventory numbers, the median home price in Yuba City continued to decline sharply. This was because the mix of sellers had changed and now included a large number of highly motivated banks selling foreclosed homes. The median home price fell to $158,700 in February of 2009.

At this point, there were three main groups of buyers;

Renters

Investors

Home owners purchasing a move up property who kept their existing home as a rental.

Over 30% of the purchases during this time were all cash. Unlike the speculators of 2004 & 2005, the investors were a positive force and helped to stabilize prices. Their business model was also entirely different than the speculators. They were motivated by rental yields that were far higher than anything available in the bank, by instability in the stock market (the massive collapse in the stock market occurred in September of 2008) and by the obvious upside potential that the real estate market offered. Real estate was a long term investment that provided a positive cash flow for them and they were not overly concerned about further price declines.

The End of The Cycle: As with the boom phase, prices at the end of the cycle are either flat or move slowly. In the three years after February of 2009, Yuba City median prices gradually declined until reaching some stability in the $140,000 to $150,000 range though there was one month at $138,205 and a low month at $129,000 in February of 2012.

The home near Queens Avenue and Stafford Way had dropped in value to about $85,000 by the end of the cycle and interest rates had declined to under 4.0%. The cost of owning that home (including principal, interest, taxes and insurance) was about $675 per month. The home near Lincoln School had declined in value to about $130,000. The cost of owning that home was about $950 per month while the cost of renting a similar home had declined from about $1,100 per month at the peak of the market to about $1,050. Rents declined only slightly from the peak of the market in 2005 to its bottom in 2012.

Most people who had purchased during the previous Boom and Euphoria phases were unable to take advantage of these lower prices and interest rates. The lucky ones were those that had obtained loans backed by Fannie Mae and Freddie Mac and could take advantage of the HARP program to refinance at the lower interest rates.

The most recent real estate cycle took 15 years to complete from its bottom in February of 1997 to its most recent bottom in February of 2012.

What Clients Are Saying

"I have nothing but great things to say about Lloyd and his wife, Tracy. They sold my home in four days and helped us get the home that we wanted. He followed up on all details above and beyond anything I expected. He has my highest recommendation. - John

Contact

Lloyd Leighton Realtors

Address: 1212 Highland Avenue

Yuba City, CA 95991-6115